Husband and I have 2 rental properties underwater about 25%, currently both are rented but for less than mortgage, both just listed for short sale. Already have an accepted offer on one between us and seller (165k, owe 203k). We are broke have no cash to repair properties. Advised I need to not pay mortgages in order to qualify for short sales. Can I keep the rent to save for future?

Also seems I need to default on CC (about 15k total on 7 cards) to trigger short sales, cause mortgagers don't believe you are in trouble unless you are in trouble across the board.

Plan to go HAFA route on primary home, because it is also underwater (at least $40K), and we want to move to a warmer climate, with our grandkids, in North Carolina. Hubby has decent job, but commute is 3 hrs round trip, and is wearing on his health, job is getting too physically demanding for him as well. We have $1600 a month in military retirement as well.

So..questions:

If we sell off small items here (furniture, pool table, old car, etc), keep cash from renters, stop paying CCs, and save as much cash as possible, can we go to NC and buy a foreclosure for cash ... I mean is it legal, not is it possible..

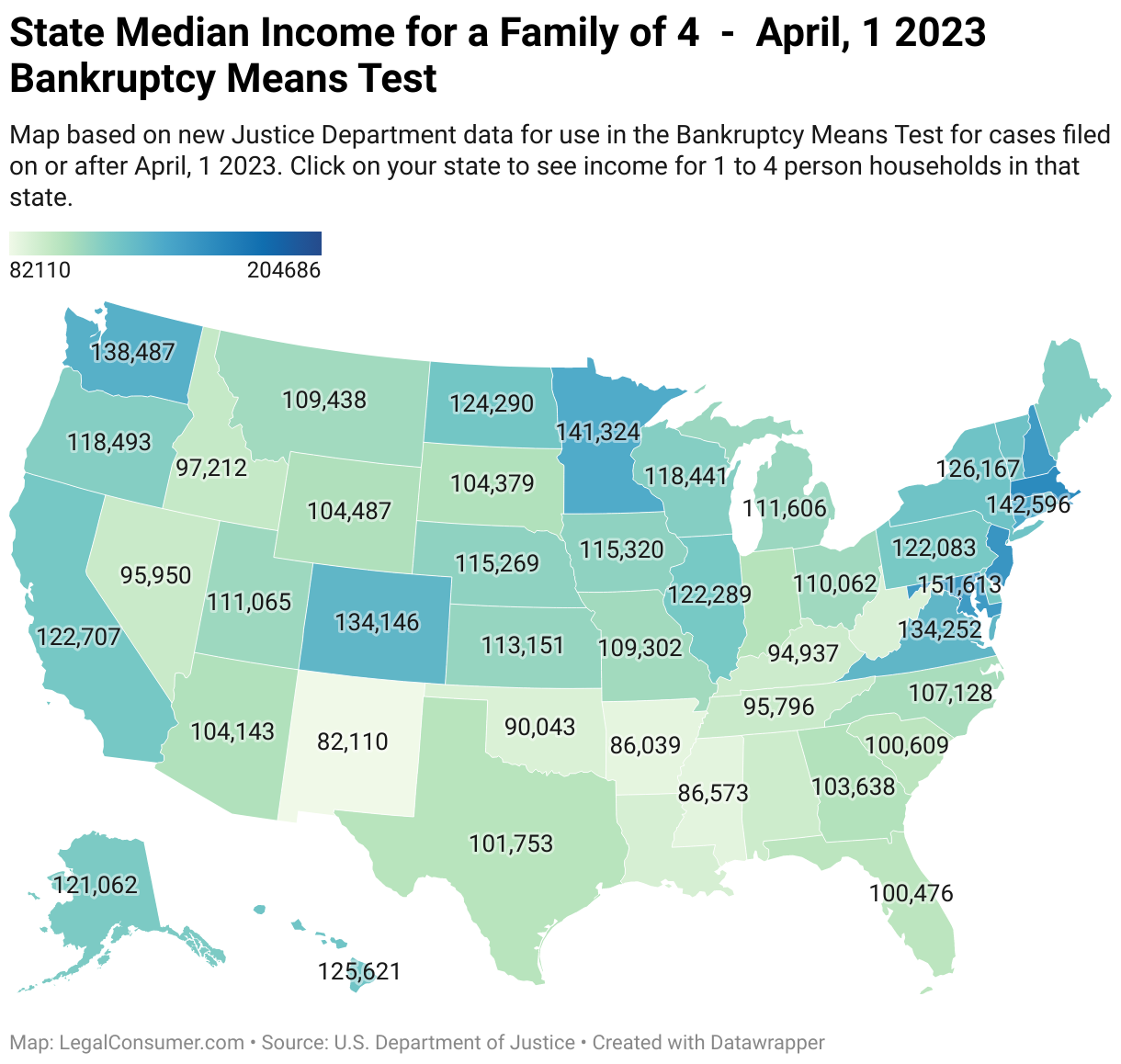

Once all houses have worked through short sale, and if we have no deficiencies, the CCs would be the only worries as far as credit. If we end up in foreclosure, we would have to file BK next year. The rental properties should allow us to go Chap 7 without means test, right? So it's okay for my husband to get a decent job?

If we do buy a house in NC, the home exemption is a total of $70k for both of us ... so if we buy a cheap house, we can convert our saved cash into a safe place, correct?

We are 55 years old, no retirement other than SS, and his military, no savings no assets, no equity, health issues, just want to go where it is warmer, cheaper, and have less stress for the years we have left...is that so wrong?

Also seems I need to default on CC (about 15k total on 7 cards) to trigger short sales, cause mortgagers don't believe you are in trouble unless you are in trouble across the board.

Plan to go HAFA route on primary home, because it is also underwater (at least $40K), and we want to move to a warmer climate, with our grandkids, in North Carolina. Hubby has decent job, but commute is 3 hrs round trip, and is wearing on his health, job is getting too physically demanding for him as well. We have $1600 a month in military retirement as well.

So..questions:

If we sell off small items here (furniture, pool table, old car, etc), keep cash from renters, stop paying CCs, and save as much cash as possible, can we go to NC and buy a foreclosure for cash ... I mean is it legal, not is it possible..

Once all houses have worked through short sale, and if we have no deficiencies, the CCs would be the only worries as far as credit. If we end up in foreclosure, we would have to file BK next year. The rental properties should allow us to go Chap 7 without means test, right? So it's okay for my husband to get a decent job?

If we do buy a house in NC, the home exemption is a total of $70k for both of us ... so if we buy a cheap house, we can convert our saved cash into a safe place, correct?

We are 55 years old, no retirement other than SS, and his military, no savings no assets, no equity, health issues, just want to go where it is warmer, cheaper, and have less stress for the years we have left...is that so wrong?

Comment