Hello Everyone. This site is amazing! I've been reading constantly for the past couple of days and already feel like I've learned so much. I'm still very stressed out though.

Here's as much detail as I can think of. Let me know if you need more info to provide accurate advice. Thanks for your help.

-2 Mortgages - 1 House we live in and the other is a rental that we loose about $200 a month on. We bought our residence about 1.5 years ago and really, really don't want to lose this house. The rental we owe maybe $20-$30,000 more on it than it's worth. Mortgage 1 is $2500/mo, Mortgage 2 is $1900/mo with rental income of $1700/mo.

-Income: I don't work (not for money anyway!). I stay home with our young kids and take care of the household, bills, etc. My husband works full time and has some side jobs he does. He probably brings in around $80,000/yr from his job and another $10-$15,000 from his side work. There are expenses we write off for the side work so it won't be quite that much.

-We have 2 cars. One is paid for but it's getting up there in miles. The other we pay around $450 a month still have 5 years left on a 6 year loan. Would need both cars so my husband can drive to work and I can run around with the kids.

-We have, I'm guessing, around $75,000 in credit card debt.

- We've been using our cards constantly for the past couple of years. I don't remember what all we've purchased but in the past few months, just small things because we literally make a payment and then use up any credit that becomes available after the principal is applied. We have made some cash advances and balance transfers. Cash advances were well over a year ago. I think we might have done the balance transfer 6-9 months ago after I got a new card and of course they are both full now.

We kept hoping that things would turn around truly thought we could afford everything but my husband's side word has gone from about $30-$40,000 a year to well under $20,000 now. We've obviously over extended ourselves with buying the house plus we charged work that's been done around the house to credit cards including a cash advance. Everything keeps snowballing and we are starting to overdraft our bank accounts and don't have the money to pay our bills. I have the money for both house payments in the bank right now and they are due today to avoid a late charge. Should I make them both? If I do, I have no money to pay any other bills for a couple of weeks.

More questions

-When should we stop paying our credit cards, or should we?

-When should we contact a bankruptcy attorney?

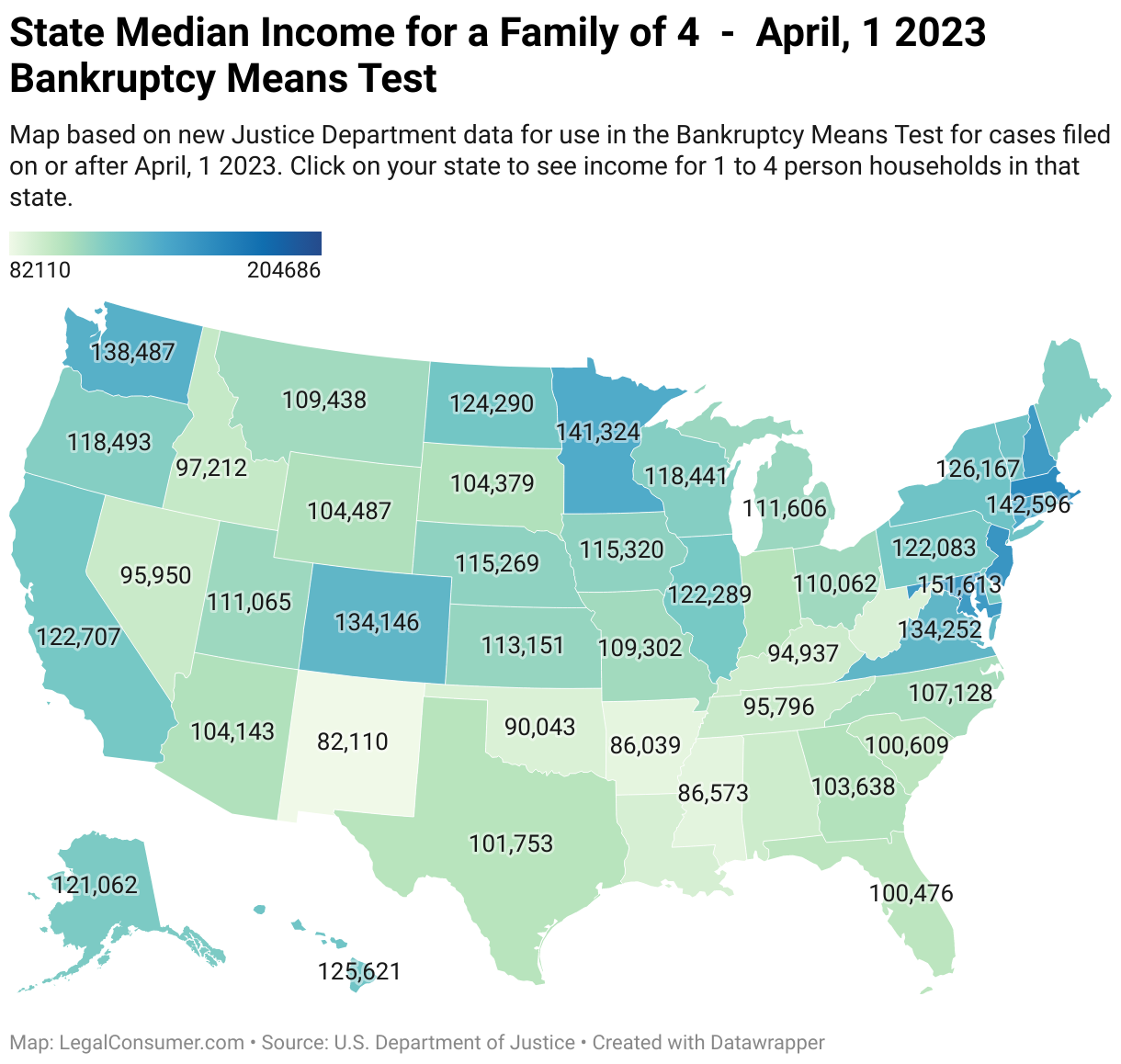

-Can we do a chapter 7? I tried to do the means test but got a little overwhelmed.

-Can we keep our primary residence? Do we keep making that payment even if we stop paying the credit cards?

-Our bank accounts are tied to auto payments for most of our credit cards. What should we do there?

We haven't done our taxes for last year yet. Kind of afraid to. My husband set it up about a year ago so that less taxes were taken out of his check so we had more money every month. We also cashed out our 401k's (except for one 401k loan) to buy our primary residence. We've always gotten a refund from the IRS but I'm afraid we may owe some this time.

That's all I can think of right now but please ask questions and give advice, it's soooo appreciated!

Here's as much detail as I can think of. Let me know if you need more info to provide accurate advice. Thanks for your help.

-2 Mortgages - 1 House we live in and the other is a rental that we loose about $200 a month on. We bought our residence about 1.5 years ago and really, really don't want to lose this house. The rental we owe maybe $20-$30,000 more on it than it's worth. Mortgage 1 is $2500/mo, Mortgage 2 is $1900/mo with rental income of $1700/mo.

-Income: I don't work (not for money anyway!). I stay home with our young kids and take care of the household, bills, etc. My husband works full time and has some side jobs he does. He probably brings in around $80,000/yr from his job and another $10-$15,000 from his side work. There are expenses we write off for the side work so it won't be quite that much.

-We have 2 cars. One is paid for but it's getting up there in miles. The other we pay around $450 a month still have 5 years left on a 6 year loan. Would need both cars so my husband can drive to work and I can run around with the kids.

-We have, I'm guessing, around $75,000 in credit card debt.

- We've been using our cards constantly for the past couple of years. I don't remember what all we've purchased but in the past few months, just small things because we literally make a payment and then use up any credit that becomes available after the principal is applied. We have made some cash advances and balance transfers. Cash advances were well over a year ago. I think we might have done the balance transfer 6-9 months ago after I got a new card and of course they are both full now.

We kept hoping that things would turn around truly thought we could afford everything but my husband's side word has gone from about $30-$40,000 a year to well under $20,000 now. We've obviously over extended ourselves with buying the house plus we charged work that's been done around the house to credit cards including a cash advance. Everything keeps snowballing and we are starting to overdraft our bank accounts and don't have the money to pay our bills. I have the money for both house payments in the bank right now and they are due today to avoid a late charge. Should I make them both? If I do, I have no money to pay any other bills for a couple of weeks.

More questions

-When should we stop paying our credit cards, or should we?

-When should we contact a bankruptcy attorney?

-Can we do a chapter 7? I tried to do the means test but got a little overwhelmed.

-Can we keep our primary residence? Do we keep making that payment even if we stop paying the credit cards?

-Our bank accounts are tied to auto payments for most of our credit cards. What should we do there?

We haven't done our taxes for last year yet. Kind of afraid to. My husband set it up about a year ago so that less taxes were taken out of his check so we had more money every month. We also cashed out our 401k's (except for one 401k loan) to buy our primary residence. We've always gotten a refund from the IRS but I'm afraid we may owe some this time.

That's all I can think of right now but please ask questions and give advice, it's soooo appreciated!

Comment