Hello all,

New here and I have a few questions. Before we get there, I will give some pertinent background information about my situation.

I am 27, live in Oregon, make roughly $3100 a month gross. No kids. My debts consist of Mortgage ($735 includes taxes and insurance), Truck loan ($505 a month, purchased in August '13 on 7 year term and am upside down at least $10k) a personal signature loan ($156 a month, 3 years left), 1 cc (about $1100 balance, $35 min payment), 1 store cc ($600 balance, $35 min payment), and one more cc with a balance of $75.

and am upside down at least $10k) a personal signature loan ($156 a month, 3 years left), 1 cc (about $1100 balance, $35 min payment), 1 store cc ($600 balance, $35 min payment), and one more cc with a balance of $75.

Basically, when I factor in my other expenses (utilities, phone, gas, insurance) I am damn near broke every month. I am sick of living paycheck to paycheck. I know what got me here (financing cars I really couldn't afford, and trading in every couple of years for something different with $0 down).

I know I am in over my head with the truck payment. If not for that, I would be able to live comfortably and still put something into savings, which currently has a balance of $0.

I do not spend frivously on anything else. I rarely eat out, and when I do it is a fast food lunch during the work week. I guess my only frivolous spending would be about $30-40 a week to play pool and have a couple beers while at the bar (I play on a league), but I have even cut that back quite a bit since last month. I only buy clothes when absolutely necessary (I literally own 3 pair of pants and a few button up shirts, and about 10 plain T-Shirts.

My only assets of any value are a motorcycle worth about $3000 that I have not been able to sell after trying several times, and a few guns totaling in value of about $2000. Beyond that, I have some crappy leather couches, a dining room table, a dresser, a fish tank, and a bed (which was purchased using the aforementioned store CC), and an older 32" flat screen TV and a PS3 I use for movies and Netflix.

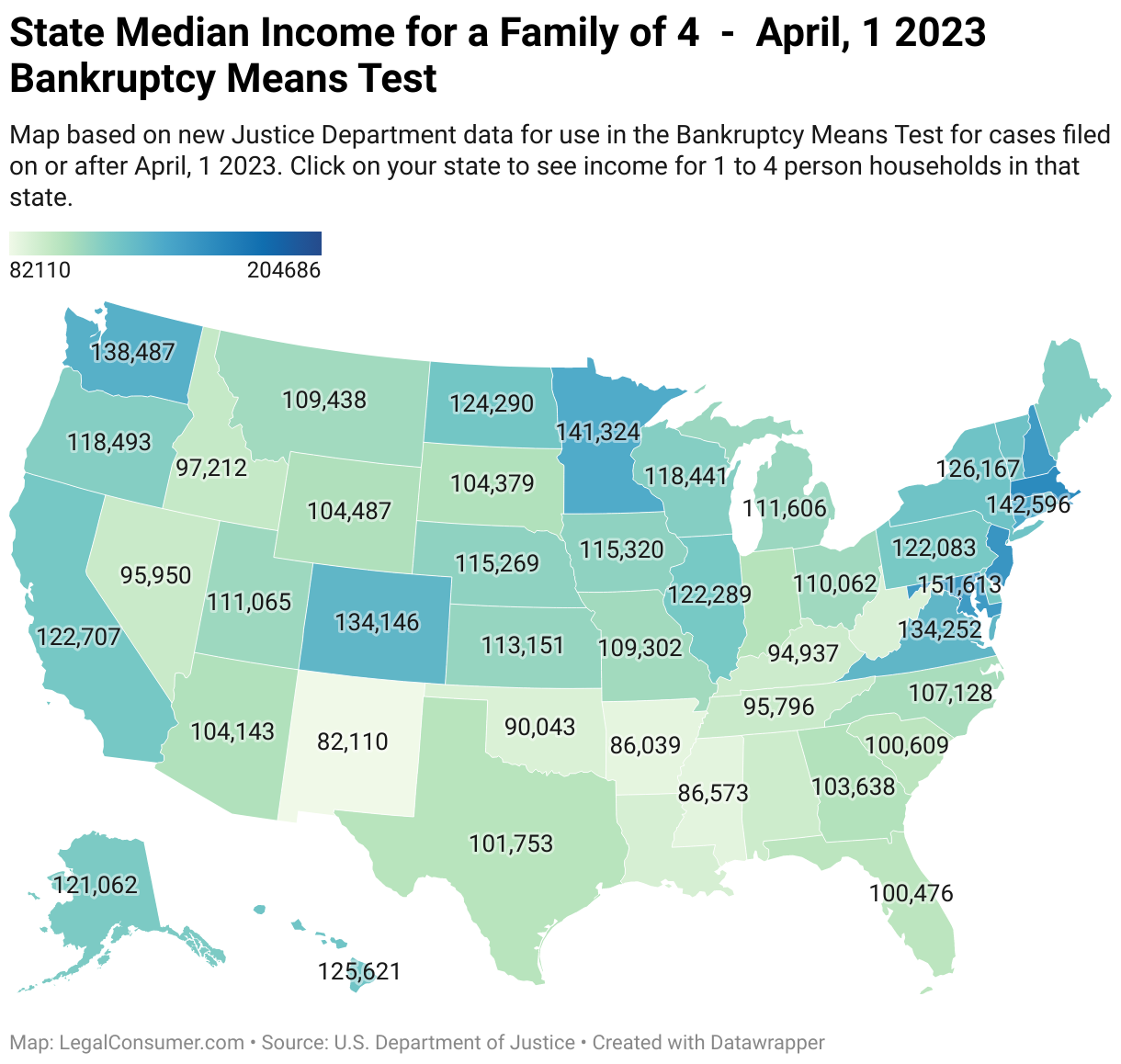

As it sits, I pass the Oregon means test, but I don't know if I have too much disposable income after removing the loans and CC from the equation. I know I need to, and plan on, visiting a BK lawyer sometime soon, but figured I'd get some opinions from others first.

Oh, I almost forgot, and just to complicate things further. My mom and my 2 younger siblings live in my home. She does not pay rent or utitlities, with the exception of Cable TV, as I did not want cable when I bought my place. I bought the house 4 years ago, and she has lived here since a week or so after I moved in. I have tried to get her to move, but due to a job loss a few years ago, it just seemed impossible for her to make it on her own and I have a hard time saying no to family. Anyway, I do not know exactly what she makes, and my siblings receive some sort of SSI after their dad passed, so this complicates things for me even more. Bottom line here, would her income be considered "household income". Her contributions to the "household" consist of groceries and cable TV, and a lot of stress and irritation! I hope to have her out by March, as she usually receives a large tax refund and I am beyond done with the current situation.

So what are your thoughts? I really do not care about keeping any of my "stuff", with the exception of 1 rifle (sentimental value more than anything) and my house. If I had to give up my other crap to get a fresh start without the stresses of high long term payments, I am 100% ok with that.

New here and I have a few questions. Before we get there, I will give some pertinent background information about my situation.

I am 27, live in Oregon, make roughly $3100 a month gross. No kids. My debts consist of Mortgage ($735 includes taxes and insurance), Truck loan ($505 a month, purchased in August '13 on 7 year term

and am upside down at least $10k) a personal signature loan ($156 a month, 3 years left), 1 cc (about $1100 balance, $35 min payment), 1 store cc ($600 balance, $35 min payment), and one more cc with a balance of $75.Basically, when I factor in my other expenses (utilities, phone, gas, insurance) I am damn near broke every month. I am sick of living paycheck to paycheck. I know what got me here (financing cars I really couldn't afford, and trading in every couple of years for something different with $0 down).

I know I am in over my head with the truck payment. If not for that, I would be able to live comfortably and still put something into savings, which currently has a balance of $0.

I do not spend frivously on anything else. I rarely eat out, and when I do it is a fast food lunch during the work week. I guess my only frivolous spending would be about $30-40 a week to play pool and have a couple beers while at the bar (I play on a league), but I have even cut that back quite a bit since last month. I only buy clothes when absolutely necessary (I literally own 3 pair of pants and a few button up shirts, and about 10 plain T-Shirts.

My only assets of any value are a motorcycle worth about $3000 that I have not been able to sell after trying several times, and a few guns totaling in value of about $2000. Beyond that, I have some crappy leather couches, a dining room table, a dresser, a fish tank, and a bed (which was purchased using the aforementioned store CC), and an older 32" flat screen TV and a PS3 I use for movies and Netflix.

As it sits, I pass the Oregon means test, but I don't know if I have too much disposable income after removing the loans and CC from the equation. I know I need to, and plan on, visiting a BK lawyer sometime soon, but figured I'd get some opinions from others first.

Oh, I almost forgot, and just to complicate things further. My mom and my 2 younger siblings live in my home. She does not pay rent or utitlities, with the exception of Cable TV, as I did not want cable when I bought my place. I bought the house 4 years ago, and she has lived here since a week or so after I moved in

. I have tried to get her to move, but due to a job loss a few years ago, it just seemed impossible for her to make it on her own and I have a hard time saying no to family. Anyway, I do not know exactly what she makes, and my siblings receive some sort of SSI after their dad passed, so this complicates things for me even more. Bottom line here, would her income be considered "household income". Her contributions to the "household" consist of groceries and cable TV, and a lot of stress and irritation! I hope to have her out by March, as she usually receives a large tax refund and I am beyond done with the current situation.So what are your thoughts? I really do not care about keeping any of my "stuff", with the exception of 1 rifle (sentimental value more than anything) and my house. If I had to give up my other crap to get a fresh start without the stresses of high long term payments, I am 100% ok with that.

Comment